ALSO IN THE NEWS

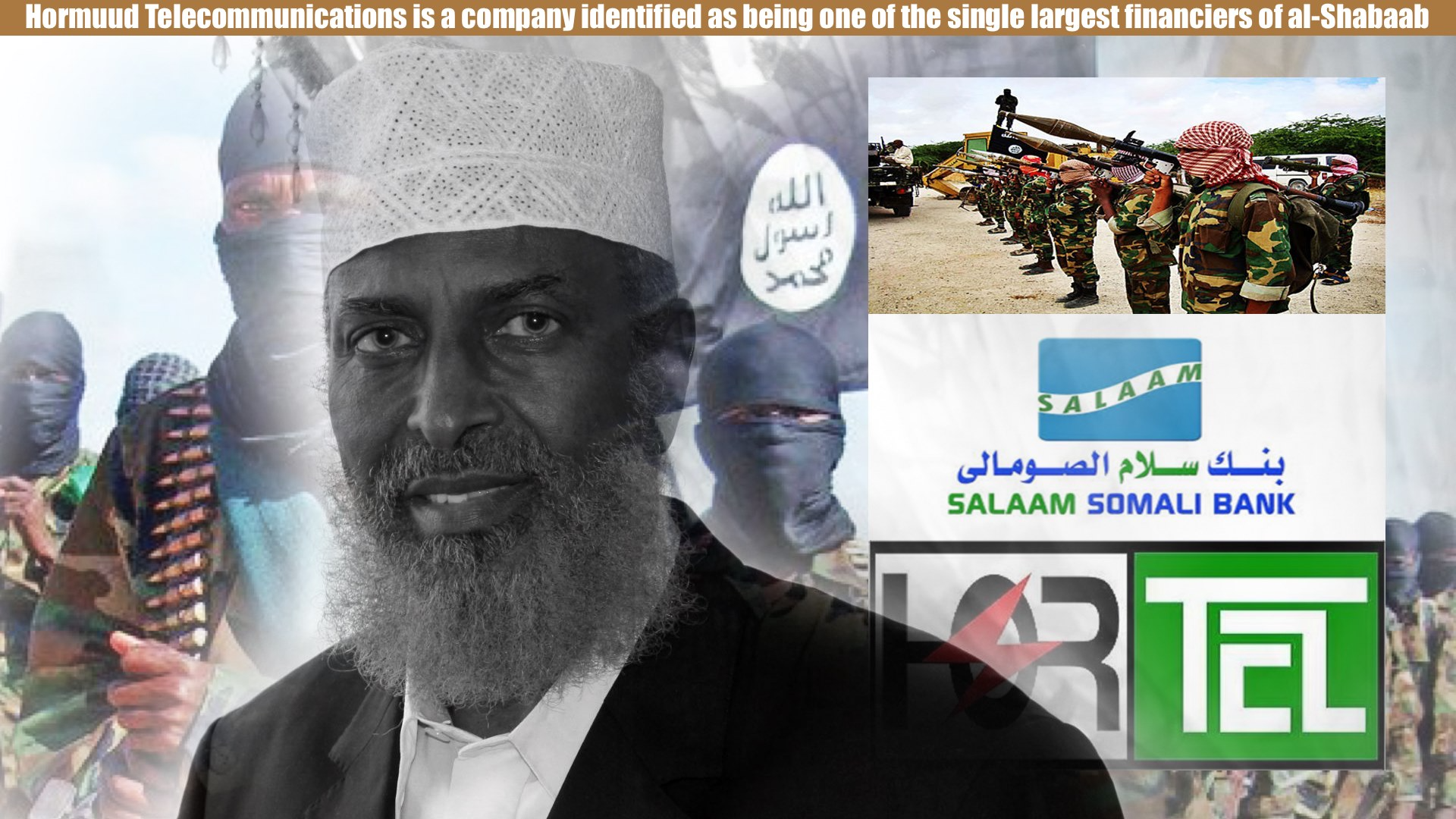

Al-Shabaab's financial system of SALAAM SOMALI BANK

0

0

Thursday October 22, 2020 - 05:27:32 in Latest News by Super Admin

- Visits: 3940

-

- Share

Countering money-laundering and the financing of terrorism

In accordance with article 14 (2) of the Somali Anti-Money-Laundering and Countering the Financing of Terrorism Act of 2016, a reporting entity must expediently report to the Financial Reporting Centre any transactions or series of transactions that appear to be linked that exceed the designated threshold of $10,000 or the equivalent in any currency. The port and zakat "taxation" accounts reviewed by the Panel recorded a total of 128 transactions of more than $10,000, all of which were required to be reported to the Financial Reporting Centre. 21

The 128 transactions of more than $10,000 reviewed by the Panel included cash deposits and direct bank transfers. Fifty-three of those transactions were made in cash. For instance, in April 2020 a cash deposit of nearly $25,000 was made into the port "taxation” account at a Salaam Somali Bank branch in Mogadishu from an individual named "A B C”, rendering the deposit difficult to trace.

Traditionally, the three stages of money-laundering are placement, layering and integration. The initial placement phase normally represents the most challenging for individuals laundering money as the origins and purpose of large cash deposits may be difficult to justify to financial institutions. The establishment of the two accounts and the investigations of the transactions made highlight the challenges that banking

Financial report received by the Panel in August 2020. $50,000 is the maximum amount of Salaam Somali Bank inter-account transfers.

Fifty transactions within the port "taxation” account spanning a five -month period and 78 in the zakat "taxation” account within a 10-week period.

institutions in Somalia face in implementing the Anti-Money-Laundering and Countering the Financing of Terrorism Act.

Mobile banking and account-to-account transfers

The port "taxation” and zakat bank accounts reviewed by the Panel were also linked to the mobile transaction service of Salaam Somali Bank, called Deeqtoon. 22 This service provided to account holders allows the transfer of funds to accounts via the Bank’s mobile telephone app. The first outgoing transaction made from the port and zakat accounts was a $5 registration fee linking a mobile telephone number to each of the bank accounts. Most importantly, this service allows for money transfer transactions between bank accounts via a mobile telephone app, up to a transfer limit of $50,000 per transaction. The usage of mobile telephones linked to bank accounts offers greater mobility and flexibility in making financial transactions. The current gaps in implementation of "mobile money” and know your customer 23 regulations result in anonymity of the controller of the mobile account, which Al-Shabaab also exploits. In its previous reports, the Panel has also highlighted Al-Shabaab’s usage of mobile money platforms for their financial transactions (see S/2018/1002, annex 2.4).

Identification documents associated with bank accounts

To open a bank account in Somalia, know your customer processes require customers to produce formal identification documents. A minority of Somalis possess the required identification documents, with over 77 per cent of the population lacking an official proof of identity.24 Investigations by the Panel found that the identification documents used to open the port "taxation” and zakat bank accounts were obtained shortly before the accounts were opened. For instance, the identity documents for the zakat account were issued through official channels four days before the account was opened.

Expenditure

Al-Shabaab’s annual operational expenditure in 2019 was approximately $21 million.25 Of that total, $16.5 million was allocated to Al-Shabaab’s military and logistical support units, with 40 per cent of the funds allocated to the purchase of weapons and ammunition. A further $4.9 million was apportioned to the Al -Shabaab intelligence arm, the Amniyat.

The four case studies investigated by the Panel (see para. 5 above) generated approximately $13 million annually for Al-Shabaab. Al-Shabaab runs multiple checkpoints across Somalia and has numerous bank accounts to facilitate i ts finances.26 The Panel assesses that Al-Shabaab is running a significant budgetary surplus.

The Panel’s investigations indicate that Al-Shabaab is investing surplus funds in various enterprises, including small to medium-sized businesses within Bakara market in Mogadishu. The review of the port "taxation” bank account highlighted two areas related to external financial investments. On 28 May 2020, $50,000 was transferred out of the port "taxation” account under a reference of " dhul lakala gatay”

__________________

See www.salaambank.so/mobile-banking.

"Know your customer” is the process of a business verifying the identity of its clients through documents such as a passport.

See World Bank, Identification for Development (ID4D) Dataset. Available at https://datacatalog.worldbank.org/dataset/identification -development-global-dataset.

Confidential report provided by a Member State, July 2020.

For additional information on Al-Shabaab checkpoints, see S/2018/1002, annex 2.4.

or "land transaction”. A total of $90,000 was transferred out of the account in four tranches for market investment referenced as "badeeco” or "market”.

Al-Shabaab's financial system of SALAAM SOMALI BANK

Countering money-laundering and the financing of terrorism In accordance with article 14 (2) of the Somali Anti-Money-Laundering and Countering the Financing of Terrorism Act of 2016, a reporting entity must expediently report to the Financial Rep